Posted on June 27, 2022

In November 2020, a report by the SADC Centre for Renewable Energy and Energy Efficiency (SACREEE); Center for Human Rights (CHR); the Boston University Global Development Policy Center (GDP Center) and others found the SADC region could potentially attain full energy access and 53 percent renewable energy (RE) installed capacity by 2040 while on its way towards zero-carbon growth. The report estimated that $52.8 billion in investment is required to meet this target.

But as a result of the COVID-19 pandemic, SADC countries have become economically vulnerable and increasingly less able to take on more external debt. Without creative thinking and new policies, this situation could derail the region’s prospects for a much-needed surge in RE capacity. Electrifying SADC countries with clean energy from renewable sources is a major regional goal, but how can it be financed when countries are unable repay existing debts or justify accumulating more debt?

Following three virtual workshops in 2021, SACREEE, CHR and the GDP Center have published a new report examining the impacts of the COVID-19 pandemic and debt distress on the expansion of RE in the SADC region and collating policy recommendations from industry experts.

The COVID-19 lockdowns were disruptive to the energy industry, with effects felt across the whole electricity value chain. RE projects under implementation were delayed due to supply chain disruptions, import restrictions and disruptions and delays in equipment procurement logistics. The immediate response to these disruptions was a shift to limited domestic production of equipment. The pandemic affected RE supply and demand in other ways as well. As people tried to escape lockdown restrictions by returning from urban to rural areas, demand for solar home systems and rooftop photovoltaic (PV) installations increased. Governments provided immediate fiscal support to utilities to keep them operational and avert further revenue loss.

Demand for electricity has gradually been returning to pre-pandemic levels, driving RE projects back into line with the region’s medium- to long-term transition pathway. The disruptions caused by the pandemic necessitated a review of the power sector’s master plans to focus on more RE both as a component of the energy mix and as a driver of national economic development.

The pandemic has caused constraints in the public finances of Africa broadly and in the SADC region, in particular. Some SADC countries have experienced declines in national revenues due to declining exports and shrinking national economies, while others are struggling with unsustainable debt and, in some cases, sovereign downgrades. The fiscal and public debt impacts, however, vary with a given country’s fiscal health. Some SADC countries were already battling with mounting public debt before the pandemic and had already substantially exceeded debt-to-GDP levels of 60 percent. It is anticipated that debt levels will only grow as a result of the continued impacts of the health crisis.

Despite the evident debt constraints caused by the pandemic and their impact on the RE sector, bankable, well-structured and financially viable projects may still attract the requisite financing. Projects already underway have mostly proceeded without interruption, possible because infrastructure project developers providing equity tend to take a long-term view of projects already under development. Additionally, some interest remains on the part of financiers and equity investors in exploring new opportunities. However, projects can fail to attract investment, as they are poorly structured and not well packaged for bankability.

The policy and regulatory environments remain a major challenge and there is evidence that an enabling environment could unlock private sector investment in the renewable energy sector, helping the SADC region reach its 2040 target of a 53 percent contribution of RE to the power mix. Policy recommendations emerging from the first workshop and section of the report on the impact of the pandemic ranged from introducing fiscal incentives to support RE development to promoting more active private sector participation through enabling regulatory frameworks, which would include redesigning market structures, strengthening regional integration, accelerating adoption of smart grids, developing more innovative financing models and shifting to more cost-based tariffs. Power sector master plans or integrated resource plans need to be revised to reflect an accelerated transition to renewable energy in line with that target.

The second workshop and section of the report documents how the pandemic has affected the sovereign and corporate debt landscape in SADC countries and has complicated the risk-assessment process of projects. While there has been some appetite and potential financing for bankable projects, it was not clear whether the pandemic’s adverse impacts on the debt landscape and on the RE sector have been underestimated. Bankability remains a key component that determined project attractiveness and a country’s debt landscape and political risk remain key considerations. While the workshop touched on various financing options, additional creative mechanisms, such as private sector financing, can supplement gaps in financing.

The third workshop and section of the report focuses on DFIs, which are well placed to both mobilize and catalyze private resources through support for mechanisms to enhance the enabling environment to better leverage private investment. National DFIs are undergoing reforms, restructurings and recapitalizations to make them more efficient. While the workshops considered how to better leverage private and equity investment, credit and currency risks—among others—are likely to drive up cost of capital, affect long term returns and eventually undermine private sector investment if the debt issue is not addressed.

The new report synthesized several key policy recommendations that could be informative for DFIs’ resource mobilisation:

Access to clean, dependable, inexpensive and readily accessible energy is essential for socioeconomic growth and development in the SADC region. Major investment gaps must be overcome by consolidating technical and financial resources, but DFIs also have a key opportunity to explore innovative approaches to financing and de-risking projects and to improve their overall contributions towards economic development.

For more information, please contact:

Dr. Magalie Masamba LL.D, LL.M, LL.B, CP3P(F)

Post-doctoral Fellow

International Development Law Unit (IDLU)

Centre for Human Rights

Tel +27 (0)12 420 5296

www.che.up.ac.za

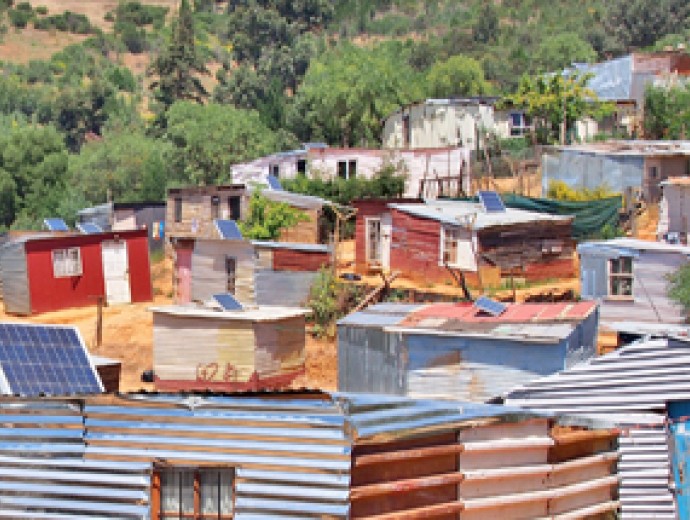

Solar panels on the roof of shack at Informal settlement - Enkanini, on the outskirts of Stellenbosch, Western Cape, South Africa

Copyright © University of Pretoria 2025. All rights reserved.

Virtual Campus

Virtual Campus

Get Social With Us

Download the UP Mobile App